The Role of Risk Appetite and Risk Culture in AML Programs

The majority of catastrophic Anti-Money Laundering (AML) failures, resulting in billion-dollar fines and institutional collapse, are seldom attributable to a lack of regulatory rules; rather, they stem from a profound failure of governance: a deficiency in how risk is perceived, accepted, and executed by the organization.

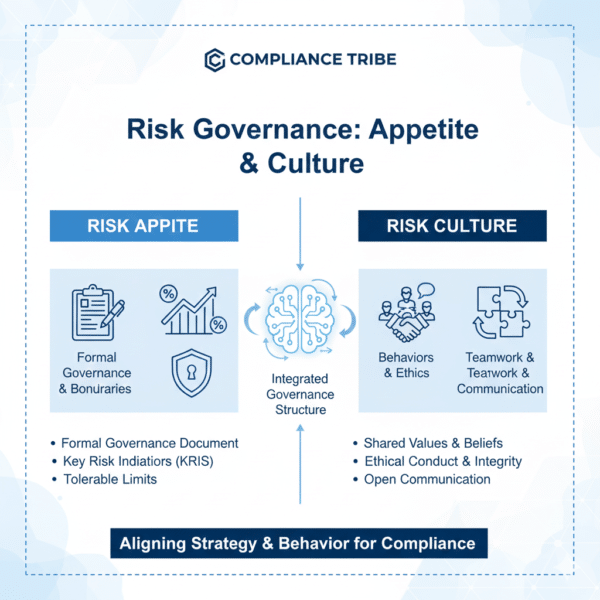

This operational integrity is driven by the Governance Twins: Risk Appetite, the formal, quantifiable limit set by the Board defining the maximum Residual Risk the organization is willing to tolerate; and Risk Culture which is the collective set of values, attitudes, and behaviors demonstrated by all employees toward compliance and control. These two concepts are the most critical drivers of a successful AML program because they determine whether compliance is viewed as an integral value or merely a bureaucratic hurdle.

Risk Appetite establishes the non-negotiable threshold that automatically mandates the necessary intensity of due diligence, if a client’s risk score exceeds this limit, they must be rejected or exited, ensuring proportionality. Simultaneously, a strong Culture ensures that front-line staff are empowered and incentivized to accurately categorize risks, perform the procedures of Enhanced Due Diligence (EDD) when required, and escalate anomalies without fear of retribution, thereby translating the Board’s strategic risk limit into consistent, day-to-day defensive action.

We’ve built a world-class AML & Compliance courses designed to elevate your career and impact. This course provides a structured approach to building an AML program. The 3-in-1 AML course offers practical foundations to implementing effective AML programs. Enroll today.

Definitions

Risk Appetite is the formal rule that says: “This is the maximum level of risk we’re willing to accept.” It’s set by the highest leaders in the company (the Board) and acts as the ultimate gatekeeper for your AML program.

It tells the company exactly where to draw the line. If a customer is found to be too risky—even after you apply all your checks like Enhanced Due Diligence (EDD)—the Risk Appetite forces you to reject them.

Risk Appetite turns subjective feelings about risk into clear, measurable numbers. You use these numbers to track things like how many high-risk clients you have, or the maximum fine you could live with, ensuring you never stray into danger zones.

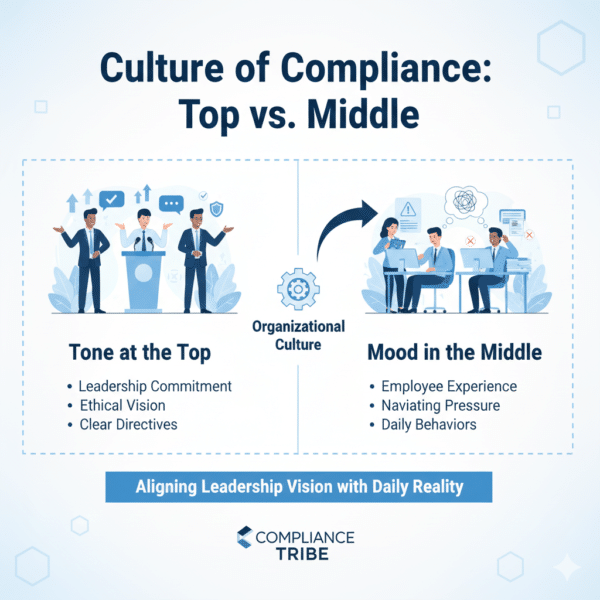

Risk Culture on the other hand is the unspoken reality of how risk is handled every day. It’s the collective attitude, values, and behavior of everyone in the company, from the CEO to the newest employee. It’s often a battle between the “Tone at the Top” (what leaders say about compliance) and the “Mood in the Middle” (what employees actually do when faced with pressure to make a sale).

A healthy culture ensures that employees see compliance as a core value, and a frustrating barrier. It empowers them to raise a red flag and challenge a risky deal without fear of getting fired or penalized. This is how the rules set by the Risk Appetite are truly enforced.

The Essence of Risk Appetite in an AML Program

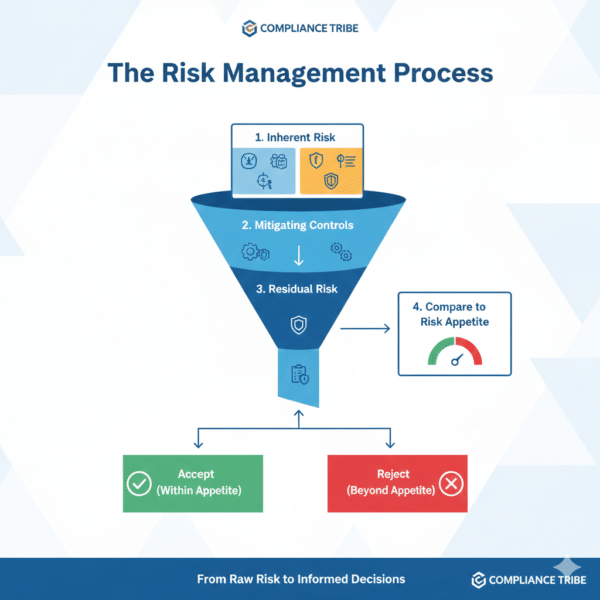

The Risk Appetite moves from a theoretical governance document into an operational tool by acting as the system’s primary filter and decision-making engine within the AML program. Its essence in action is to enforce the Risk-Based Approach (RBA) with absolute objectivity, ensuring that the institution’s exposure is always proportional to its defined tolerance.

1. Client Acceptance and Rejection (The Gatekeeper)

The most direct action of the Risk Appetite is establishing non-negotiable acceptance and rejection criteria during client onboarding and review. Once a client’s Inherent Risk is assessed and all mitigating controls (like EDD) are applied, the final Residual Risk Score is checked against the appetite. The appetite sets a maximum permissible score; if the client exceeds this benchmark, the business unit is obligated to decline the relationship. This process prevents subjective sales pressure from overriding strategic risk policy, ensuring the firm only onboards clients whose risk profile fits within the Board’s acceptable tolerance, thereby safeguarding the institution from undue exposure from day one.

2. Driving the Tiered Due Diligence Model

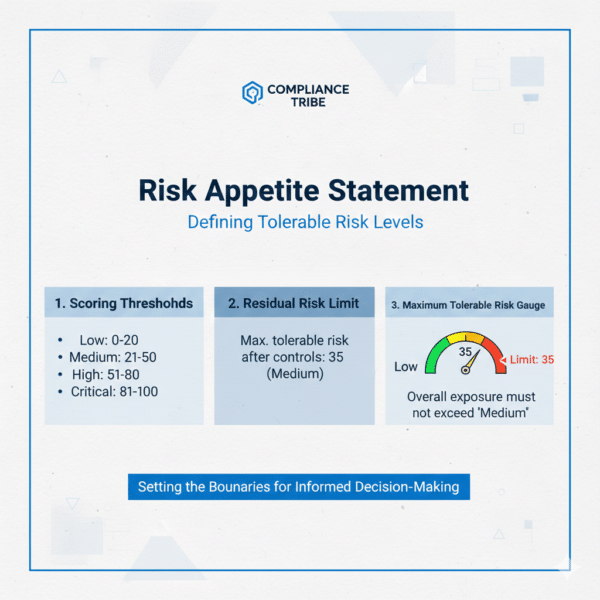

Risk Appetite directly operationalizes the RBA by defining the precise numerical thresholds for the tiered due diligence model (SDD, CDD, EDD). The appetite pre-defines which risk score range (e.g., 0-30, 31-70, 71-100) corresponds to which level of scrutiny. This removes ambiguity: a client scoring 72, which is defined as “High-Risk” by the appetite, automatically and non-negotiably triggers the full suite of Enhanced Due Diligence (EDD) actions, including Source of Wealth (SOW) verification and senior management approval. This stratification ensures proportionality; that compliance resources are applied intensively only where the appetite demands it, thereby optimizing efficiency while meeting the legal standard of care.

3. Setting Strategic Business Limitations

The appetite functions as a strategic document that limits commercial activity in areas deemed excessively risky, regardless of individual client profiles. It dictates which products, services, and geographies are entirely off-limits because their inherent risk is too high to be mitigated back to an acceptable residual level. For example, the appetite may explicitly prohibit any engagement with businesses linked to certain sanctioned jurisdictions or services known for extreme anonymity (like specific crypto products or bearer shares). By setting these hard boundaries, the appetite protects the integrity of the overall client portfolio and ensures the institution avoids sectors where the cost of control and the risk of failure are simply too high.

4. Triggering Ongoing Control and Exit Strategies

Risk Appetite governs the continuation and termination of client relationships. A high-risk rating dictated by the appetite requires more frequent and intense Continuous Monitoring (e.g., weekly transaction review instead of monthly). The appetite also defines the mandatory off-boarding threshold. If an existing customer’s behavior changes (e.g., triggering repeated Suspicious Activity Reports) and their subsequent review score pushes the Residual Risk back above the maximum limit established in the appetite, the firm must initiate the process to terminate the relationship. This ensures the ongoing portfolio remains compliant with the Board’s tolerance and prevents risky clients from lingering due to inertia.

We’ve built a world-class AML & Compliance courses designed to elevate your career and impact. This course provides a structured approach to building an AML program. The 3-in-1 AML course offers practical foundations to implementing effective AML programs. Enroll today.

The Essence of Risk Culture in an AML Program

The Risk Culture is the institutional foundation that determines the fate of the entire AML program; it is where the strategic policies set by the Board are either rigorously executed or carelessly dismissed. Its essence in action is ensuring that every employee’s daily decision aligns with the organization’s formal Risk Appetite, turning abstract governance into concrete defensive behavior.

1. Driving Proactive Escalation

A strong Risk Culture creates the necessary psychological safety that empowers employees, especially those on the front line (tellers, sales associates), to act as the institution’s first line of defense. This means staff feel confident and incentivized to escalate potential red flags or transactional anomalies, even if it risks delaying revenue or inconveniencing a high-value client. This proactive behavior is critical, as it ensures that suspicious activity is not buried or ignored due to internal pressure to meet sales targets, directly counteracting a dangerous “revenue-over-risk” mentality.

2. Eliminating the “Tick-the-Box” Mentality

In a weak culture, staff fall into the trap of a “tick-the-box” approach, performing the absolute minimum required by procedure (e.g., collecting a single ID) without engaging in critical thinking or verifying data independently. A functional Risk Culture combats this by emphasizing the purpose of the control, not just the action. Training focuses on explaining why Enhanced Due Diligence (EDD) is mandatory for certain clients and what the ultimate criminal risks are, ensuring staff understand that they are safeguarding the firm, not just following arbitrary rules. This embeds a culture of skepticism and due care.

3. Aligning Incentives and Accountability

Culture actively works to reinforce compliance by aligning internal incentives. If a sales manager is compensated solely on the speed of client onboarding, they will pressure staff to bypass CDD or EDD steps. A strong culture fixes this by ensuring accountability is tied to compliance metrics. This involves senior management modeling the desired behavior—demonstrating a commitment to exit a profitable client if their Residual Risk exceeds the Risk Appetite, thereby showing employees that integrity truly outweighs short-term gain.

4. Continuous Reinforcement and Measurement

Risk Culture isn’t static; it requires constant effort. In action, this means regular, targeted training that goes beyond annual online modules and addresses specific, recent AML typologies or internal control failures. Furthermore, a firm with a strong culture actively measures the culture itself, using employee surveys, compliance feedback loops, and audit findings to assess the “Mood in the Middle.” This continuous feedback ensures that leadership can immediately identify and correct areas where compliance is being compromised by commercial pressure or operational negligence.

Integrating AML Risk Appetite and Culture in an AML Program

Integrating Risk Appetite and Culture means ensuring the strategic limits set by governance are faithfully executed by every operational employee. If these two elements are misaligned, the entire AML program can fail.

1. The Alignment Imperative (Bridging the Gap)

The central function of integration is to ensure that the Risk Appetite document is not only a regulatory filing, but also a living guide that informs behavior. A strong Risk Culture acts as the bridge between the Board’s stated risk tolerance and the front line’s daily decisions. If the appetite prohibits onboarding high-risk clients from a sanctioned country, the culture must ensure that a sales team, even under pressure, honors that prohibition and feels empowered to decline the relationship without internal consequence. Integration requires that every employee understands their role in protecting the organization’s approved risk level.

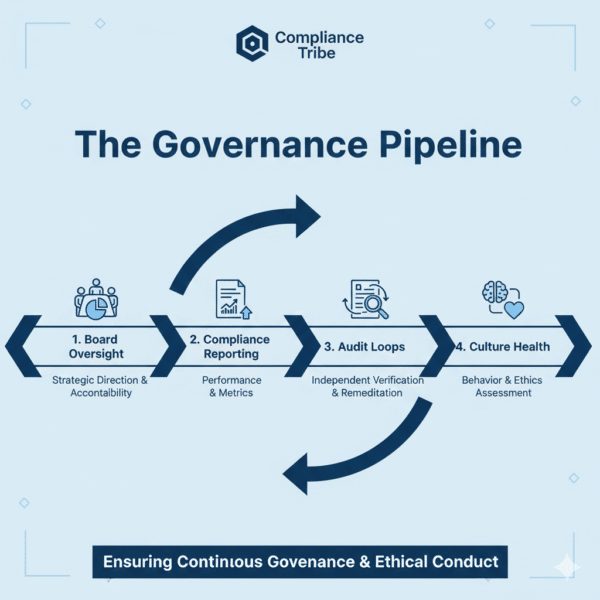

2. Governance Oversight and Review

Integration is enforced through active governance. The Board and senior management must establish robust processes to monitor and measure both the appetite adherence and the cultural health.

- Appetite Review: Compliance must regularly report to the Board, showing key metrics (e.g., aggregate high-risk client count, Suspicious Activity Report volumes) to confirm the firm’s current Residual Risk remains within the documented appetite. If metrics exceed the appetite, the Board is obligated to intervene and mandate a change in controls or business strategy.

- Cultural Measurement: Institutions must actively measure the culture itself, perhaps through anonymous employee surveys that gauge their confidence in escalating issues or their perception of management’s true priorities. A healthy integration means audit reports rarely find procedural shortcuts stemming from commercial pressure.

Consequences of Disintegration

When the Risk Appetite and Culture break apart (Disintegration), the result is catastrophic compliance failure.

- Regulatory Non-Compliance & Massive Fines: The most immediate consequence. If the Risk Appetite states no Residual Risk above X, but the weak Culture allows sales staff to onboard clients scoring X+1, the firm has violated its own documented policy. Regulators treat this as a governance failure, leading to larger fines than if the appetite simply didn’t exist.

- Compromised Enhanced Due Diligence (EDD): A weak culture undermines the integrity of controls. Staff, under pressure, will bypass or shortcut the rigorous verification steps (like verifying Source of Wealth) required for high-risk clients, nullifying the firm’s attempt to reduce its inherent risk and directly exposing it to money laundering.

- Inconsistent Risk Decisions: Without a unified culture, different business lines or branches will interpret the same Risk Appetite limits differently. This ruins the entire Risk-Based Approach (RBA), leading to a patchwork of controls where some areas are overly cautious and others are dangerously lax, creating exploitable soft spots for criminals.

- Erosion of Employee Trust: When staff see leaders preach compliance (Tone at the Top) but reward sales teams who break the rules (Mood in the Middle), it destroys confidence. Employees become disincentivized to report suspicious activity, knowing they might be penalized for slowing down revenue, ultimately paralyzing the internal control system.

- Irreparable Reputational Damage: Major AML scandals are frequently rooted in cultural failures. When news breaks that a bank knowingly ignored its own risk limits (the Appetite) due to a profit-hungry culture, public, investor, and correspondent bank trust is immediately lost, often leading to severe restrictions on business operations

In conclusion, the efficacy of an AML program is a direct reflection of its governance, proving that major compliance failures aren’t about lacking rules, but about the disintegration between policy and execution. A successful defense hinges on the alignment of the Risk Appetite, the Board’s quantitative limit on exposure, with a strong Risk Culture that empowers every employee to rigorously apply controls like Enhanced Due Diligence (EDD) and reject risky business, thereby ensuring the final Residual Risk remains acceptable. Failing to integrate these two concepts is an open invitation for regulatory fines and reputational disaster. Don’t let internal dysfunction be your firm’s biggest weakness: Enroll in our comprehensive AML Internal Control course to master this governance structure, or contact our consulting division today to inquire about bolstering your corporate AML posture and aligning your culture with your risk strategy.