Understanding The Customer Due Diligence Process

Customer Due Diligence (CDD) is unequivocally the bedrock of any effective AML strategy, serving as the critical first line of defense against illicit financial activities that plague the global economy.

Regulated entities, particularly financial institutions, are not merely encouraged but mandated by global standard-setters, such as the Financial Action Task Force (FATF), and local bodies like the U.S. Financial Crimes Enforcement Network (FinCEN), Central Bank of Nigeria (CBN), to establish robust CDD processes to verify customer identities and assess associated financial crime risks.

In this article, we will explore what Customer Due Diligence (CDD) is, its primary objectives, the tiered approach to CDD, the core processes of CDD and why continuous monitoring is important in the CDD lifecycle.

Definition

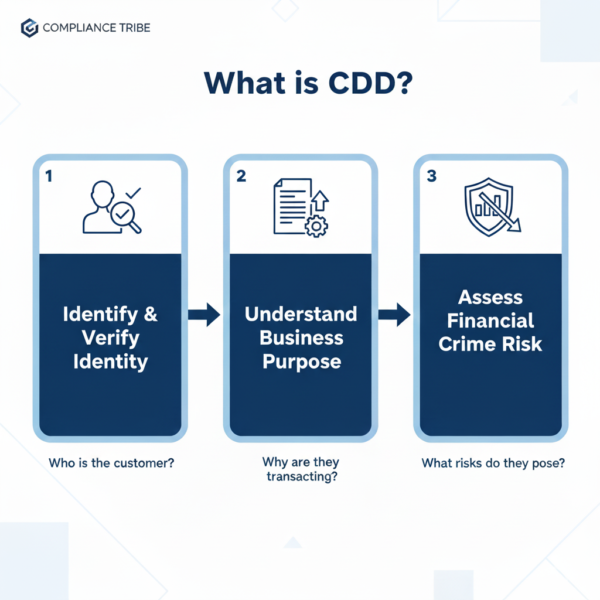

Customer Due Diligence (CDD) is the mandatory, risk-based process that forms the foundation of AML compliance. It requires regulated entities to systematically perform three core functions:

- Identify and verify the customer’s true identity (including beneficial owners).

- Understand the nature and intended purpose of the business relationship.

- Assess the level of financial crime risk the customer poses (low, standard, or high).

Customer Due Diligence(CDD) is not a one-time onboarding exercise; it establishes the essential baseline of expected activity, enabling institutions to conduct continuous monitoring to detect and report suspicious deviations from the customer’s verified profile.

The Primary Objectives of CDD

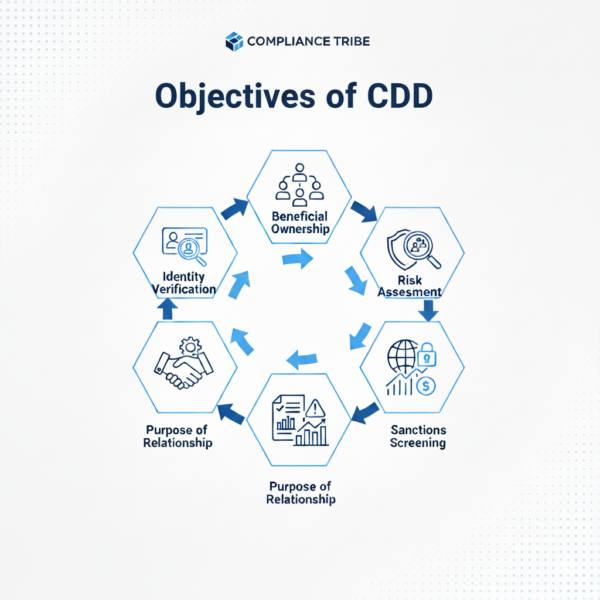

The robust function of Customer Due Diligence (CDD) is realized through six interconnected objectives designed to maintain transparency and control financial crime risks throughout the customer lifecycle:

- Identity Establishment and Verification (IEV): to identify and verify the customer’s legal identity using reliable, independent source documents, ensuring they are not operating under a pseudonym or stolen credentials.

- Beneficial Ownership Identification: For corporate and legal structures, this involves identifying the ultimate natural persons who own or control the entity (typically 25% or more), thereby preventing the use of complex structures to conceal criminal control.

- Risk Assessment and Rating: The goal is to evaluate the inherent financial crime risk posed by the customer based on factors like their geography, business sector, products/services used, and Politically Exposed Person (PEP) status. This results in the assignment of a formal risk rating (e.g., Low, Standard, High-Risk).

- Purpose and Relationship Understanding: Determine and understand the legal and commercial rationale for the customer seeking the financial relationship, including their stated source of wealth and source of funds. This establishes the necessary context to determine if future transactions are legitimate.

- Sanctions and Watchlist Screening: A dedicated objective is to screen the customer and associated parties (like UBOs and directors) against all relevant global sanctions lists (e.g., OFAC, UN) and watchlists immediately upon application and periodically thereafter. This ensures compliance with foreign policy and antiterrorism laws.

- Establishing an Activity Baseline for Monitoring: The goal is to collect sufficient data to build a pattern of expected transactional behavior (e.g., expected volume, type, and geography of transactions). This baseline is indispensable for the continuous monitoring phase, as any deviation from it will trigger an alert for potential suspicious activity.

The Tiered Approach to CDD

Every customer requires due diligence, but effective AML compliance mandates a risk-based approach. This translates into a three-tiered CDD framework that scales the intensity of scrutiny to match the customer’s risk level.

This tiered framework, comprising Simplified Due Diligence (SDD), Standard CDD, and Enhanced Due Diligence (EDD), allows financial institutions to allocate resources efficiently, focusing minimal efforts on low-risk customers while dedicating greater scrutiny to high-risk relationships.

This systematic differentiation ensures regulatory proportionality and optimizes the defense against sophisticated financial crime.

1. Simplified Due Diligence (SDD)

SDD is the lowest level of scrutiny applied to customers who present a demonstrably low risk of money laundering or terrorist financing.

- When It Applies: SDD is typically permitted when the customer or the product carries a low inherent risk. Examples include:

- Government public bodies or state-owned entities.

- Companies listed on recognized stock exchanges (as they are already subject to disclosure requirements).

- Low-value, limited-function services (like pre-paid cards with strict spending limits).

- Action Taken: institutions may apply fewer or reduced verification measures. This might involve:

- Reduced frequency of periodic reviews.

- Verifying identity with fewer documents.

- Collecting less information on the purpose of the account.

- Key Principle: While SDD simplifies the process, it does not eliminate the requirement to identify the customer. The institution must always justify why a customer was categorized as low-risk..

2. Standard Customer Due Diligence (CDD)

Standard CDD is the mandatory baseline level applied to the majority of an institution’s customer base—those who fall within the normal, expected risk profile.

- When It Applies: This is the default requirement for all new customers unless they qualify for SDD or, conversely, trigger the need for EDD.

- Action Taken: Standard CDD involves fully executing the six primary objectives we just discussed, including:

- Verifying identity using reliable, independent source documents.

- Identifying Beneficial Ownership (if applicable).

- Screening against sanctions and watchlists.

- Establishing the source of funds and expected activity baseline.

- Key Principle: Standard CDD ensures the institution has sufficient information to confidently assert who the customer is and understand their financial profile.

3. Enhanced Due Diligence (EDD)

EDD is the highest level of scrutiny reserved for high-risk customers or transactions, requiring deeper investigation and ongoing monitoring.

- When It Applies: EDD is triggered by specific, higher-risk factors that increase the potential for money laundering. Examples include:

- Politically Exposed Persons (PEPs), their family, or close associates.

- Customers operating in high-risk geographic jurisdictions (as defined by FATF or local regulators).

- Businesses dealing in high-risk sectors (e.g., casinos, high-value art dealers, or complex international trade).

- Situations where the complexity or size of the transaction is unusual.

- Action Taken: EDD requires measures beyond standard CDD, such as:

- Collecting additional independent verification sources.

- Obtaining senior management or compliance officer approval for onboarding.

- Verifying the specific Source of Wealth (SOW), not just the source of funds.

- Conducting more frequent and intensive continuous monitoring.

- Key Principle: The core objective of EDD is to reduce the high inherent risk to an acceptable residual risk level before the relationship is approved.

By implementing this tiered system, institutions ensure they focus their limited compliance resources where the risk is greatest, optimizing their defense against financial crime.

The Core Processes of Standard CDD

While the tiered approach dictates the level of scrutiny, the core processes of Standard CDD are the specific, non-negotiable actions that must be taken for the majority of average-risk customers.

These core processes can be organized into three essential stages:

1. Customer Identification Program (CIP) and Data Collection

This process is focused on gathering the foundational information required by law to establish the customer’s legal existence.

- Action: Collecting all required identifying information from the customer.

- For Individuals: Name, address, date of birth, and identification number (e.g., passport, national ID).

- For Entities: Business name, physical address, incorporation documents, and tax ID number.

- Key Deliverable: Obtaining documentation to confirm the identity of any Ultimate Beneficial Owners (UBOs)—the natural persons who ultimately control or profit from the entity.

- Goal: To establish a full, verifiable profile of who the customer is and who controls them.

2. Verification and Screening

This stage ensures the data collected in the first stage is accurate and that the customer is not on any prohibited lists.

- Action: Using reliable, independent sources to verify the information provided by the customer.

- Verification: Cross-referencing government-issued IDs, utility bills, or corporate registration documents.

- Screening: Checking the customer and their UBOs against two key areas:

- Sanctions Lists: Global watchlists (like those from OFAC, UN) to prevent transacting with prohibited parties.

- Adverse Media/Watchlists: Checking for connections to criminal activity, corruption, or terrorism (Negative News Screening).

- Goal: To confirm identity authenticity and flag immediate legal or reputational risks.

3. Understanding and Risk Profiling

This final stage of Standard Customer Due Diligence (CDD) connects the customer’s identity to their anticipated financial behavior, preparing the file for ongoing monitoring.

- Action: Collecting information to understand the rationale for the customer relationship.

- Source of Funds (SOF): Understanding where the money being used in the initial transaction or account funding originated (e.g., salary, sale of property, inheritance).

- Purpose of Relationship: Documenting the expected type, volume, and geographical reach of transactions (the Activity Baseline).

- Goal: To establish the customer’s initial risk rating (usually Standard) and create the benchmark against which all future transactions will be measured during the continuous monitoring phase.

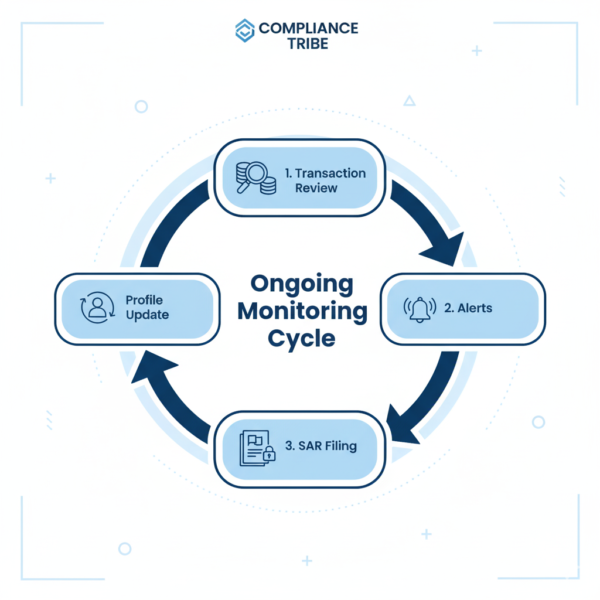

Continuous Monitoring

Continuous Monitoring (CM) is the essential, long-term phase that transforms Customer Due Diligence from a one-time event into an ongoing operational requirement. It is the mechanism by which a financial institution ensures that the customer’s risk profile remains accurate and consistent throughout the entire business relationship.

This concept revolves around two main areas of perpetual scrutiny:

- Transactional Monitoring Against the Baseline: Continuous monitoring systems automatically and retroactively analyze all customer transactions. Their primary function is to compare the customer’s real-time financial activity (e.g., deposits, transfers, frequency, and geography of payments) against the Activity Baseline established during the initial Standard CDD process. If a transaction or pattern deviates significantly from what was expected (e.g., a low-risk client suddenly receives a massive international wire transfer inconsistent with their known income), the system generates an alert, which requires immediate human investigation and potentially the filing of a Suspicious Activity Report (SAR).

- Customer Risk Profile Maintenance: CM is also responsible for ensuring the customer’s identity and status are perpetually up-to-date. This includes automated and periodic screening of the client against global sanctions lists, checking for negative news or adverse media reports, and confirming that the beneficial ownership structure of corporate clients has not changed. The frequency of this continuous review is directly tied to the risk-based approach: high-risk customers (subject to EDD) are monitored daily or weekly, while low-risk clients may only be reviewed annually.

In essence, Continuous Monitoring is the operational safeguard that protects the institution by ensuring that if a legitimate customer turns bad, or if a criminal attempts to use a clean account for layering illicit funds, the deviation is detected and acted upon swiftly.

Conclusion

To sum up, Customer Due Diligence (CDD) is the non-negotiable process that anchors the entire AML framework, moving from the initial collection and verification of identity to the sophisticated, tiered assessment (SDD, Standard, and EDD) of risk. By establishing a robust baseline through defined core processes and maintaining constant vigilance via Continuous Monitoring, institutions ensure they always know who they are doing business with, effectively guarding against financial crime throughout the customer’s lifecycle. Don’t leave your firm exposed to escalating threats and regulatory penalties. Secure your expertise today: Join the priority waitlist for our essential KYC course to master these processes, or contact our consulting team now to inquire about bolstering your corporate AML posture and ensuring ironclad compliance.

Good content